Update Dec 14, 2024: Added Newsletter Email Archive at End of Post.

Exchange Rates Introduction

Recently, I have had been lucky enough to go travelling through some countries in Europe and paying for things in a different currency gets one thinking about economics, naturally. To start of my discussion I’m going to mention my visit to Edinburgh because last time I was in the UK it was July of 2022 and I noticed that the exchange rate was significantly different than it is today in September 2024. Back in 2022 the exchange rate was about 1.5 CAD to 1 GBP. This time it was closer to 1.8 CAD to 1 GBP. Basically, it got more expensive for me, but if you think about this on a surface level, currency rates are somewhat of a silly thing. I haven’t changed much, the amount of money that I make hasn’t changed much. On an individual level it’s kind of weird that at different points in time if you want to go and travel, the value of the money you make in your home country can decide the types of things that you can do and how expensive your vacation will be. With so many countries accepting your credit card it makes exchange rates feel even more fake. For example, I was in Denmark and I didn’t see a single Danish Kroner. I couldn’t tell you what that currency looks like, it didn’t even occur to me to exchange money before I went over there because everyone accepts cards. When money is digital it’s somewhat funny to me that there’s different “currencies” at all, it’s just numbers on a screen.

Why Currencies Strengthen or Weaken

Getting past the fact that digital payments are a somewhat funny concept, let’s talk about how the strength of your currency is determined. The different currencies and exchange rates are mostly based on your home countries economy. But this encompasses many things. Employment rates, inflation, Gross National Product, health of trading partners, imports/exports, government policies, etc. All currencies are technically free markets, this means that the market for your countries currency could hypothetically react to a bad piece of news and the currency could temporarily strengthen or weaken, sometimes significantly, on a single news story. Often, there is also a comparison going on, generally the benchmark is the United States, the European Union and various other large economies which are the benchmarks for healthy economies which other currencies are compared against. You may notice in your home country that there is inflation or it’s harder to find a job for a large part of the population, or foreign governments are not buying your governments bonds because the interest rate they are paying is lower than a competitors government. There are a lot of economic dynamics that can determine the value of your currency compared to the currency of another country.

Example of Bad News Affecting Exchange Rates

Let’s take the time that I went to the UK in 2022, arguably, it was a great time to travel to the UK because around that time the country was having governmental problems and their prime minister at the time was ousted, then an interim prime minister was given power, proceeded to break everything by implementing policies everyone agreed were horrible, then was ousted in a matter or weeks or months, all I remember was that a piece of lettuce lasted longer than the PM. These terrible policy decisions led to a loss of confidence in the UK, not quite as crazy as Brexit was, but this period of instability meant that the British Pound took a nice little fall, it was temporary, but the recovery wasn’t immediate. At that time buying British pounds from a foreign exchange perspective would have been a great time to do so since the country itself is largely stable, but this was just a temporary moment of instability. Now, one could argue, that we are getting closer to what the historical exchange rate was. I remember prior to Brexit the British pound was closer to 2.1 CAD to 1 GBP. There’s no saying if it will ever return to that value since Brexit is quite a permanent decision. But we can look towards other interesting economic indicators to get an idea of what exchange rates might look like in the future.

Canada’s Dollar Will Weaken in 2025

For Canada, unfortunately, the Canadian dollar is anticipated to weaken a little bit more in the coming year 2025, which means travel will become more expensive, and arguably makes now a good time to buy foreign currencies such as the USD or the GBP. So why is the Canadian dollar predicted to be weaker? There are a few reasons. Canada is beginning to see quite a jump up in the unemployment rate, people are continuing to lose jobs and new jobs are hard to find. Fewer jobs means fewer people spending money, less demand for goods, less goods produced, this slowing becomes a cycle and our economy “slows”. Since employees are basically business investment, and business investment leads to production or exports/imports. If there is less business investment, and fewer people working, it generally follows that the GDP or GNP of Canada will decline. Another reason this is problematic for Canada is because in the US the GDP has actually been climbing and they are our largest trading partner, so by comparison, we are doing worse, and our currency suffers. Additionally, Canada still has a largely resource based economy, with the largest one being Oil, and Oil prices have not been as strong in recent months, you may see this as a good thing since it’s cheaper to buy gas at home, but it does cause our currency to suffer somewhat. All of these problems, and inflation finally coming down led to the Bank of Canada to cut interest rates in an attempt to stimulate the economy.

Interest Rates, Bonds, and Currencies

Canada was notably the first G10 nation to cut rates. The country has now cut rates three times with another rate cut anticipated before the end of the year. Cutting interest rates means it should in theory be easier for businesses to get loans and invest back into producing goods and get consumers spending again since their loans will also be cheaper, this may also increase housing activity in Canada, which is also a huge part of the economy. But in the interim, our currency will likely suffer while we try to increase output because fewer people will want to purchase Canadian government bonds since the Fed in the United States has yet to cut their rates, making their bonds a more attractive place for people to leave their money. When the government sells bonds, it takes money out of circulation, meaning there are fewer dollars, which means less inflation, less inflation usually leads to a stronger currency. We did somewhat benefit from this since our inflation wasn’t as high as the United States during covid so we had a stronger currency for a while, but the US continues to surprise with their economic output, the machine continues to operate well, while Canada’s is suffering a bit at least from an economics point of view.

Conclusion

In conclusion, Canadians can expect travel to become a bit more expensive over the coming year or two, with the future TBD. I think we need to be pushing to improve investment in technology companies, so much of the world relies on tech and our only claim to fame is Shopify. Economics are a complex problem, and tech won’t solve all of our issues, but we do need to find a way to benefit from the knowledge that we have in the country, because we also suffer from a pretty significant brain drain, the best and highest paying jobs are in the US for our smartest students, so most of them will naturally decide to go there. The US is a great country if you have lots of money and good benefits, and if something goes wrong while they are there, they can always come back, it’s sort of a win-lose for Canadians and Canada. The best way for a Canadian to start a tech company is to move to California, at least last time I checked, so that needs some fixing. This will be a bit of a shorter post because I’m technically on vacation. Currently, I’m sitting outside a coffee shop called Przystanek Kawa in the wonderful Dutch inspired old town square of Gdańsk, Poland (bit of a mouthful, but the city is beautiful), and I’m going to get back to being a tourist and enjoy the sights. I’ll be in Warsaw tomorrow, then it’s off to Lauterbrunnen before returning home (sadly). I will say this solo travel thing does sort of get old quickly (this is only day 2 of 7 days solo) especially when you’re in a place where you aren’t speaking your first language, you can only see so many museums, castles, and church’s before it all starts to feel the same, and hostels have their own quirks and problems, definitely have some stories for another time about rough roommates. Anyway, it’s easy to complain, but I’m extremely happy and lucky that I can do this kind of travel even if it’s not high class luxury travel, I’m quite enjoying the experience and continue to love each new city I go to. That’s all for now, see you in Canada!

Newsletter Email Archive Sent: September 16, 2024:

Newsletter #21: Exchange Rates in A Digital Economy, August Real Estate Stats

*Bank of Canada Cuts Rate 0.25%, now sits at 4.25%. – Sept 4, 2024

TRREB August Market Stats Summary:

September has arrived, marking the near end of summer with kids heading back to school and holidays wrapping up. Seasonally August tends to be a slower month of the year when it comes to residential real estate sales. The Greater Toronto Area home sales were down on a year over-year basis with the region’s housing market remaining well-supplied in August. Currently there are approximately 4.5 months of inventory, putting us in what is referred to as a Buyers Market.

The Bank of Canada announced a further rate cut on September 4th which will lead to improvement in affordability. Buyers today are more sensitive than ever to changes in borrowing costs as they pay close attention to what their monthly mortgage payment could be. As mortgage rates continue to trend lower this year and next, we should experience an uptick in buying activity, including in the condo market.

There were 4975 home sales reported by the Toronto Regional Real Estate Board(TRREB) throughout the month of August 2024 – down by 5.3% compared to 5,251 sales reported in August 2023.

Inventory of all home types available for sale were up 46% compared to August of last year, there are currently 22,653 properties for sale. With this jump in inventory you would expect downward pressure on pricing, however, prices remained flat over August 2023 influenced by lowering interest rates and the continued strong demand to live in the Greater Toronto Area. The average selling price was down only 0.7% compared to August 2023 to $1,074,425.

TRREB’s Chief Market Analyst Jason Mercer stated that as borrowing costs trend lower over the next year-and-a-half, home buyers will initially benefit from both lower monthly mortgage payments and lower home prices. Even as demand picks up, especially in 2025, it will take time for the inventory of listings to be absorbed. Ample choice in the market will help keep price growth moderate for the foreseeable future.

Stock Market:

The Fed will cut rates soon, this is already priced into the market, but it’s likely to cause a bit of a temporary happy bump as money becomes a bit cheaper. Getting housing activity moving again will be a sign of a more affordable rate environment as many people in the US do not want to exchange a 30 year fixed mortgage at 2 or 3 percent for a more expensive one at 6 or 7 percent.

Market Performance as of Monday September 16, 2024:

Canada CPI Inflation July 2024: 2.5% (0.2% Decrease from June 2024) Current BoC Benchmark Interest Rate: 4.25% (0.25% Decrease on Sept 4, 2024) Unemployment Rate June 2024: 6.4% (0.2% Increase from May 2023)

Update Dec 14, 2024: Added Newsletter Email Archive at End of Post.

Why People Invest in Commercial

The commercial real estate rabbit hole is never ending. Depending on the situation commercial real estate can also provide better returns than residential real estate partly due to the fact that commercial real estate out the gate is viewed as an investment with a profit motive. Therefore, the only other people you are likely going to be competing against are other investors. Whereas investing in residential is a bit different because you are also competing with people who view it as a place to live not just a way to make money. Therefore, they may be willing to pay more in order to get what they want, meanwhile investors generally speaking are looking for a great deal, a high ROI, and may have a shorter timeline than someone who plans to live in their home for years. The owner/occupant might view paying a premium as a small price to pay for a great house they’ll live in long term.

Does Multi-Family Count as Commercial?

Before diving into the various categories of commercial real estate and the pros and cons of each and what to consider before investing. I want to talk about a category of commercial real estate that is sort of in-between commercial and residential, and that is multi-family commercial. Multi-family commercial is generally 6 or more units, this category of commercial also tends to be competitive with respect purchase prices. In larger cities cap rates (I’ll explain this in a minute) tend to be lower because if there is demand for rental units (e.g. big city = demand), the investment will provide a fairly consistent return without much vacancy or lost rent. Many investors who started out purchasing residential real estate as an investment will frequently work their way up to multi-family apartment buildings once they have the funds to do so, and may even get into construction and development or re-development.

More Competition in Multi-Family Space

However, as mentioned, there can still be quite a bit of competition for these kinds of investments. Although not as much as a typical residential home. On a quick tangent here, in the Greater Toronto Area multi-family investments are becoming harder and harder to find because we simply aren’t building purpose-built rentals anymore (another name for multi-family). In an attempt to make everyone feel like an owner, we have been building almost exclusively condo apartments, which tend to come with high costs, unnecessary expenses, and don’t tend to be all that affordable. Therefore, the price of purpose built rentals as investments have gone up (as have rents) in larger cities. In an attempt to alleviate some of the stress from underbuilding purpose built rentals are conversions of larger homes to 3+ units. This has become very easy to do thanks to recent changes in housing regulations, up to 4 units on a single lot. This presents opportunities for investors who have some skill in construction management, but they may still find it challenging to make the investment work due to the sheer amount of competition from owner/occupants who also want to purchase those homes. However, the amount of converted homes will likely increase over time as investors become more adept at doing conversions and homeowners themselves begin to add additional suites. This could also make these homes become worth even more thanks to the extra income, everyone seems to want an “in-law” suite. So the regulations could really benefit the investors or owners who are able to purchase and upgrade their homes which could benefit supply. But overall we won’t be able to exclusively rely on this method of adding housing supply as it really is a small drop in the bucket compared to building purpose built rental apartments like we did back in the 70s and 80s. Ok, now back to what you came for, talking about other kinds of commercial real estate.

Offices and The Pandemic

Firstly, lets discuss office buildings. If you’ve been following the news in the past 3 years or so we had a small little pandemic. The effects of the work from home shifts that were caused due to the pandemic, meant that a lot of office spaces were sitting vacant for a long period of time. Workers and companies moved to a hybrid model. Then all of a sudden they didn’t need as much space as before. Even the most expensive, sought after real estate 1 World Trade Center in Manhattan had some of it’s tenants downsize and sublease their rentals because they weren’t using the space anymore. The effects for smaller landlords in smaller cities were more significant. From an investors perspective, the high vacancy that office real estate has seen presents a big risk, if you choose to invest, you could face long vacancies and it could hurt your profitability, or ability to pay the bills. However, where there are problems there is also opportunity. Because of the high vacancy rates, you could purchase a “distressed” asset at a very good price (whatever that means in your market), and then come up with a plan to change its use, or change the type of professionals that you cater to. I’ve heard of people renovating their buildings and turning them into co-working spaces, residential apartment buildings (can be a big investment since fire code regulations tend to be different when kitchens and sleeping are involved) and various other conversions. I’m sure you’ve seen some of those old industrial buildings that get converted into extra high ceiling apartments with a rustic feel, generally called lofts, although people can be pretty loose with that term nowadays. But for the right person, and for the creative investor, an investment in office real estate right now presents a TON of opportunity.

Get Your Starbucks Out for Retail

Secondly, what about retail. Now that’s something you don’t think about. But yes, someone (or usually a company) owns shopping malls. Generally those large individual businesses that occupy them don’t own the real estate. They rent out the space as do other various businesses and due to a good location, or modern amenities or what have you, businesses lease the space and try to turn a profit of their own. Investing in retail real estate can be quite a bit more involved and may also require more scrutiny on what types of tenants you want and the tenant mix you are looking for. As an investor in retail, you have to take a different approach and you almost have to view the space you are leasing as a partnership with the businesses that will occupy them. Likewise, if your retail space is subpar, a tenant may choose not to rent there because they may be worried about the sustainability of their business. Both landlord and tenant in a retail situation benefit from a few main components. Traffic through the area. Are there lots of people? Are residences being built nearby? Is there a highway that people often pull off from? Are there any “anchor” tenants: these are tenants like your Walmarts, Tim Hortons, Starbucks, Big Grocery Stores etc. which drive traffic to the area. If you can get good anchor tenants, this may also attract other tenants to the area. Anchor tenants tend to have more bargaining power due to the fact that they will likely contribute a significant portion of the traffic. Economic forces are also a factor, if we look at the pandemic again there was a time and there were many businesses who went out of business because they were either unable or not allowed to operate their in-person stores. This is unlikely to happen again, but people’s expectations have changed and if businesses aren’t changing in line with expectations they could become irrelevant before long.

Light Industrial: Warehouses etc.

Thirdly, probably the most complicated form of investment in real estate, light and heavy industrial. Light industrial is a bit easier to manage, but may still require special considerations. Light industrial involves things like warehousing, small time manufacturing, and other types of businesses that involve warehouses to some degree. This could just be a kitchen, bath, tile warehouse, Costco and IKEA could both fall under light industrial, but since they are also retail it might be sort of complicated to categorize. Depending on the type of tenants that are interested in renting out this real estate you may have to make certain adaptations to the property, or the tenant may request adding more power or maybe a ceiling crane, or other larger things that are used in warehousing. In some ways this type of real estate can be easier to manage, but because every tenant will likely have different requirements you may end up spending a lot of time with engineers to see if the property can be adapted to what they are proposing.

Heavy Industrial: Probably Irrelevant for You

Heavy industrial on the other hand is extremely specialist, and frequently the companies involved in this type of work will just buy the land themselves when possible. This involves things like chemical plants, oil refineries, car manufacturing facilities etc. The big consideration for investors who are thinking about buying land that was previously used as a manufacturing facility is environmental concerns. Land has to pass multiple layers of inspections by the EPA (Environmental Protection Agency) here in Ontario. Often they will require remediation of the land before it can be used again or the land can be sold and remediation costs can go from hundreds of thousands to millions of dollars depending on the damage and requirements of the EPA. So once you start getting into industrial, environmental issues become more of a concern. On a smaller scale it is important to keep in mind environmental concerns when you are purchasing ANY commercial real estate that was either on or around a gas station, a mechanic shop, dry cleaner, certain farming operations, or any other business that heavily uses chemicals. You don’t want to find out when it’s too late that you have to remediate land. So it’s always advisable to research what prior businesses were nearby and to put in a clause to get the land inspected by the EPA prior to agreeing to purchase it. Next I’ll dive into what to do after purchasing land, and how commercial leases differ from residential.

The Commercial Property Lease vs. Residential

With all the examples of commercial real estate above we should talk about leases, since they can be quite different than what a residential investor is used to. First of all, the minimum lease term is generally 5 years with 10 year leases also being common. The screening for commercial leases tends to be more intense, since landlords are expecting the tenant to survive at least 5 years if not longer. The landlord will frequently pass on all the operating expenses of the building. But the tenant may also be able to negotiate that the landlord pitch in on some renovations to get their business operating quicker. There are all kinds of technical terms for commercial leases, generally a triple net lease (or net net net lease) is one where the tenant covers all expenses including large ones such as roof repairs, property taxes, snow maintenance etc. A single net lease (or net lease) is one where the tenant is responsible for it’s portion of utilities and the landlord takes care of the building etc. There is also double net leases, but these terms are somewhat loose and each agreement will be different.

Additionally, in most leases the tenant is able to make whatever renovations they want to a unit, there may be a stipulation that they have to return it to a certain state when they move out. But any renovations are usually the tenants responsibility (unlike in residential where the landlord renovates units for the tenants). Furthermore, there is no such thing as a “standard lease” in commercial real estate, the way that there is in residential. This means that generally a landlord can put whatever conditions they want in a lease, so it is important to read it in detail and have a lawyer review it.

Calculating Rent and Realtor Fees

Note that the realtor fee tends to be a percentage of the total lease which is usually the landlords responsibility to pay. I should also mention that if you are looking to rent commercial space, you will likely have noticed that the way the lease price is presented is quite different from residential. Rather than a per month amount, the price is per square foot. For premium downtown Toronto office real estate (Class A buildings) you may be looking at $40 per square foot, for suburbs it might be closer to $20 per square foot. Just as an example, lets say the space you want to rent is 1000 sq ft offered at $20 per square foot. When you multiply the numbers you get $20,000. That $20,000 would be the annual rent plus any other additional fees agreed to by the landlord and tenant. Each year, the price may change. So in year 1 it might be $20 PSF, then by year 5 it may go up to $25 PSF.

Calculating Square Footage, Useable vs. Non-Useable

Commercial real estate is also a bit strange in some ways because a portion of the common area may count towards the total sq ft that you are renting, this is usually the landlords responsibility to take care of for all the tenants in the building. But it won’t be useable sq ft for operating your business. So you need to make sure if you require a certain amount of useable space that you confirm and measure the space yourself and figure out how much of the sq ft the landlord is asking you to rent is common area square footage. This extra square footage may change your willingness to rent a certain space or to pay a certain price for that space. The idea for renting “non-useable” space is that it’s a nice lobby area for clients to wait in, or its a foyer that makes the building look nice at the street level, and it’s a value add to your business. Some businesses may see it as a value add, others may not.

Capitalization Rate or Cap Rates:

You’ll probably hear cap rate about a million times when you’re looking at commercial real estate as an investment. Essentially a cap rate is what the market requires the property to generate as a return on investment and determines the property value (most of it anyway). For multi-family residential in Downtown Toronto for example a 4-5% cap rate would be considered good. For example, lets say my multi-family building generates $80,000 net of expenses each year (operating income). Let’s also say the generally accepted cap rate in the area is 5%. You take the 80000/0.05 = 1,600,000 is the value of the property. Alternatively, let’s say someone is asking 2,000,000 for a property that generates 90,000 of income. You can find the cap rate by dividing 90,000/2,000,000 = 0.045. So the cap rate is 4.5% for this property.

Analyzing Your Commercial Investment

You do have to be careful when you are investigating a property since naturally the owner will do whatever they can to make it look as good as possible. Owners should have documents of all the expenses of managing the property as well as the rent rolls and vacancies of the property. Sometimes, they don’t and you’ll just get a bunch of estimates. Regardless, it’s important to do your own research and make your own estimations of how much the expenses would cost. Are there some changes, investments, or upgrades that you can make which will improve the cap rate of the property after purchasing? What are the opportunities available that the previous owner didn’t bother to take advantage of? This type of thinking is essential to making a good investment, because usually the market price of a property and the potential of that property can be quite different. It is also frequently the case that the current rents of the property will not cover the cost of financing so to make the investment work you will have to think creatively.

Internal Rate of Return (IRR) and Net Present Value (NPV)

There are other metrics that investors use as well, such as IRR, or internal rate of return, this takes the investments cash flows, purchase and sale price over a longer time horizon and gives an expected rate of return. Sometimes investors will go into an investment with the expectation of a certain IRR. If the investment meets the IRR, then they will go ahead, if not, they will pass. IRR is frequently used as a discount rate in calculating another number called the net present value (NPV). NPV is a way to discount future cash flows factoring in a discount rate. The discount rate, can be based on many things, generally the risk free rate (the rate that government bonds are paying) plus some other factors such as mortgage rates (the value you could get lending the money to someone else) and inflation (time value of money) are taken into account. Using a formula all the expected future cash flows are discounted using the discount rate and they yield a dollar amount. If the dollar amount is negative factoring in the discounted cash flows, this means that the investment will likely be worse than an equivalent risk free investment. If the value is positive it means the investment is better than a risk free investment (or it meets the investors required IRR). Generally the rule of thumb is that NPV has to be zero or higher to move forward with an investment. My explanation is not great, but I do have a video that does a better job explaining these things below, if you’re ready to dive into the technical weeds:

Property Management, Systems, and Employees

Lastly, what about management? Depending on how you set up your rentals you may need to hire an admin staff to manage it, cleaners to keep common areas or business offices in tip top shape, and have some tradespeople you trust to fix things when they break. As you build up a portfolio it might make sense to hire a property manager who manages everything. From finding new tenants to hiring the tradespeople and cleaners. For almost all types of real estate investing once you get to a certain level, property management becomes very important. There are property management companies which provide the service for a fee (usually around 10-20% of rent). This might make sense for you if you have one or two properties. But if you have a larger portfolio there comes a time where it makes sense to hire an employee to do this for you.

If you choose to go down this route, you’d be well advise to have a handbook that has phone numbers of tradespeople you trust, and step-by-step approaches on what to do in certain situations (or “systems”). It will be a lot of work, and you’ll learn as you go, but having a “run my life manual” can be extremely helpful for the people that work for you, and saves you the headache of having to approve a small expense, or screen every tenant, or deal with every small leak or lightbulb. I think building out this type of “systems” or “operations” manual early on is a very good idea, that way when you hire someone, or an employee leaves, you aren’t left hanging with no direction to give this person. Obviously, some situations are different but you can get as low level as you want, including the types of brands you trust or don’t trust when replacing broken components. Building something like this will make your life much easier before you hire someone, and will make the employees life easier when you eventually do.

Why Commercial is Worth it (Conclusion)

In conclusion, believe it or not this was a very brief and very light overview of how investing in commercial real estate works. The goal of my post was just to get you thinking about it and to somewhat de-mystify it. A lot of people will never invest in commercial real estate, or don’t even think about it, but it is frequently a better investment than residential real estate. But as with any thing that provides a higher return there is higher risk. It’s very mainstream to invest in residential real estate nowadays. The barrier to entry for commercial is a bit higher, and usually when there is a higher hurdle to jump over, that is the opportunity you should chase because it will keep your competition out. Simply by the fact that it’s a bit more challenging. Residential is quite frankly oversaturated with investors and the gaps in the market are very slim to the point where the only way to make those investments work now is to take on a lot more risk and oftentimes without a suitable upside.

No matter how you swing it nowadays, getting a profitable investment is going to take some work, and I hope that by bringing your attention to commercial real estate investing you might be interested in learning more about it. If you do I would highly recommend the b real estate podcast, they have a ton of episodes talking about commercial real estate, it is American so some of the rules will be different to Canadian rules. But just getting an understanding of the various ways people get creative with their investments is a huge leg up on the competition. Additionally, I would recommend talking to someone who is a commercial real estate owner and investor, they can be a bit harder to find, and I would recommend trying to find someone who is still active in their investments because they will likely have had to face recent hurdles that will be helpful to learn from in todays market. I’m also certain that there are Canadian real estate podcasts out there which have episodes talking to investors and they’re definitely worth checking out as well. As my final word of parting, if you do nothing else, you should just get started. People spend way too much time (myself included) over researching and reading for months or years without taking any action. Preparation is good, but don’t forget to put the things you learn to work! Thank you for reading and as always.

Keep investing,

Oliver Foote

Newsletter Email Archive Sent: August 21, 2024:

Newsletter #20: Investing in Commercial Real Estate, Fall Real Estate Market Expectations

This Weeks Blog Post:

Investing in Commercial Real Estate: Retail, Offices, Industrial, & Multi-Family:

Why people invest in commercial real estate

What the various types of commercial real estate differ

How to calculate commercial real estate numbers, why to think about investing in commercial

Hopefully everyone has enjoyed their summers, it’s crazy how quickly they went and how quick September is looming just around the corner. I hope that you were able to have some fun this summer and that you’re feeling refreshed from some time off.

Last months TRREB numbers showed that the current interest rate cuts were not having a significant impact in buyer activity. I believe that this trend will continue and that it will take some more rate cuts for first time buyers to get back into the market. There is a lot of supply on the market and it will continue to build up this September. There is another rate decision coming September 4 and I’m inclined to think that the bank of Canada will want to cut rates again. Employment numbers are continuing to be lackluster here and in the US and this gives reason to me to continue bringing rates down.

Business growth on the whole is currently sitting in a “maintain” state as many buyers for discretionary services or businesses are cutting back causing the overall demand of the market to drop. So if you are in business and are maintaining your revenue numbers right now, you are probably gaining market share on the whole since the size of the market is shrinking.

Just hearing through the grapevine, the employment situation is a bit worse than the numbers would make it seem. People are continuing to get laid off from their jobs as companies are still trying to focus on efficiency at lower cost. Some positive trends are that net food prices (after sales) are continuing to come down. Gasoline prices seem to have stabilized and rent prices appear to also be stable or dropping in some places. Simply because we aren’t formally in a recession doesn’t paint the whole picture. Life has become a lot harder for a lot of people, and everyone is somewhat worried and not spending money like the crazy spending we saw during the pandemic. The “stress” on the economy is being felt by everyone.

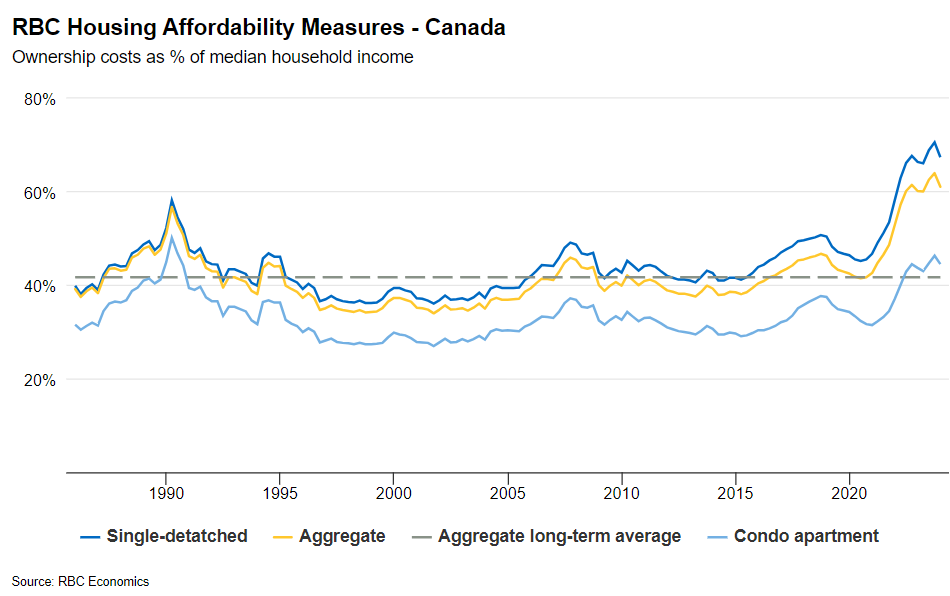

One of my favourite charts to judge the state of housing affordability is this chart from RBC, this was published July 4, 2024, and shows a very moderate improvement in housing affordability. But it is still considered quite unaffordable for most, which again points to more rate cuts from that perspective.

Stock Market:

Lastly, 2 weeks ago I wrote about how employment numbers in the US caused a dip in the stock market, and how I said it was likely very temporary. Well two weeks later we’re right back to where we were before the dip. Quite short lived.

Canada CPI Inflation June 2024: 2.7% (0.2% Decrease from May 2024) Current BoC Benchmark Interest Rate: 4.50% (0.25% Decrease on July 24, 2024) Unemployment Rate June 2024: 6.4% (0.2% Increase from May 2023)

Update Dec 14, 2024: Added Newsletter Email Archive at End of Post.

The Modern Challenge of Finding a Career:

Many young people, myself included, have a hard time trying to figure out what to do with their lives. I’m usually a proponent of try as much as you can until you find something that sticks, but this is much harder to execute in reality than it may initially seem. Changing from thing to thing to thing can be exhausting in the same way that just sticking with the first thing you find and end up hating going into work every day is exhausting. So what is the answer? If doing something you hate is exhausting, and trying to find something you love is exhausting, what are you supposed to do? That’s the topic I’m going to try and tackle today. Not necessarily an easy topic to discuss, but I think I have some insights that may be somewhat helpful to the directionless or those who want to change direction.

Why “Do What You Love” Sucks:

I’m first going to start with the common wisdom of “do what you love.” I’ve been hearing this for quite some time, and after trying to do just that, I actually think this statement is backwards and that “do what you love” is not great advice. Why? Well if you’ve ever tried to make a living off a hobby that you enjoy doing in the few spare hours off work, you’ll quickly learn that making money, and doing something for fun, for most of us, are two different worlds. When you try to make money off something you are doing for fun, it can often cease to be fun, and I think this is especially true for creative endeavours. If you are a painter, or you make trinkets or cookies in your free time, and you try to mass produce paintings and trinkets, you’ll soon find yourself burnt out from needing to paint every second of the day in order to keep up with the demand for your art (best case scenario). If you aren’t accustomed to the pace of painting all day long, and you don’t have a way of continuing to make it interesting for yourself, you may find yourself no longer interested in that thing. There are those few people in the world who make a living off their music, or their art, or some other creative endeavour, but there are thousands and thousands more who are “starving artists.” So unless you have an unrivaled thirst to out practice and outwork basically every single competitor, or some unrivaled business acumen, you might want to continue doing that thing as a hobby.

Why You Shouldn’t Start a Business Based on “Do What You Love”:

I spoke in my pervious article (Employed Vs. Self-Employed Work) about what people overlook when they are starting a business, and I discuss the huge challenges with being self-employed. If you do choose to “do what you love” as your own business, you need systems in place, you’ll spend a lot more time just managing the business than you want, and you’ll have to become a jack of many trades rather than being able to focus on your craft. This can be managed and software nowadays is a godsend, but I still caution people who want to leave stable work for effectively contract jobs because you really are going to be working 24/7 rather than just 9-5. I see these advertisements for Realtor school quite often on my Google ads (presumably because I spend a lot of my time looking at houses and economic data), and I always laugh at their tagline “escape your 9-5, take control of your own schedule”. Which loosely translates to, “you’ll now be working 9-9 most days, oh also doing open houses on weekends, and if you’re doing this business right, you’ll likely be fielding calls or making calls most hours of the day. You’ll have to try and find new business every day and you’ll spend the majority of your time just looking for clients rather than working for them.” If you want something to be completely engaged in, then by all means, do the self-employed game, maybe you’ll love it, but if you want balance in your life, maybe don’t. You can create some amount of balance once you’ve established yourself, have a client base, and know how to delegate, but at the start you will be working your butt off to make ends meet with lackluster results unless you’re truly exceptional. Usually it takes people 5-10 years before they can slow down a bit and take back some control of their schedule, and some people never manage to. So, don’t say I didn’t warn you.

How Building Your Skills Leads to Love:

Now, I’m going to somewhat contradict the above paragraph. Because I’m going to talk about the right way to “do what you love”. Since I mentioned this phrase is backwards you’re probably wondering what I think is the right phrase. I think it’s something along the lines of “work hard, learn a skillset, do disciplined practice, become an expert, and finally, love the result.” It’s so much easier to love something you’re good at, that you’ve practiced at, and that you want to keep pushing the boundaries in. This perspective is not new to me, but it has been reinforced by a few books I’ve been reading recently the first is The Algebra of Wealth by Scott Galloway, which I think is a great introductory finance book and money book in general. The second is Grit by Angela Duckworth (a bit late to the party I know). I think that both of these books overarching ideas when it comes to a career is focusing on becoming good at the thing you are doing, and reframing “failure” as something that helps you get better and better.

It’s Supposed to Be Hard:

Often when you are learning something new, it’s going to be hard, it’s going to suck, and you’re going to want to quit. In Grit Duckworth interviews many Olympic swimmers and one of them says (I’m paraphrasing), “honestly, going to practice is hard, and I frequently don’t want to go, and I often find myself thinking about quitting.” She then goes on to say that a top performer attitude is doing the hard thing anyway. They are focused on the top level goal of getting to the Olympics and winning medals. They have a compass that guides all of their lower level motives. She stresses the importance of finding your one overarching life compass that doesn’t change. When it comes to putting in the hard work that is hard to do every day, she stresses the importance of routine. It’s much easier to do the hard thing if you have a routine and do it at the same time every day, so you don’t have to “re-convince” yourself to do the hard thing. Just showing up is half the battle. Lastly, the importance of long term commitment. The good old 10,000 hours (or 10 years) of practice to become an expert is something that can be hard to remember when you’re in the trenches doing the hard work, but nothing replaces disciplined practice. Probably the most important trait or feeling you need to have towards the work you are trying to do is the desire to be constantly getting better. If you have no drive or “grit” to improve on the last thing you did then you’ll quickly lose the motivation you need to keep moving. This is where other people are extremely helpful and getting quick feedback on what you’ve done is extremely important too. You should have a coach or mentor figure who can help you set goals for disciplined practice, and then can give you feedback on what you’ve done so you can improve quicker. You should also spend some time reflecting on your practice and resting, don’t overdo it every single day. Even Olympic athletes have a daily training limit. If you do all these things, and are focused on challenging yourself, building a skillset though putting in multiple repetitions, getting feedback, and have an compass guiding your lower level goals. Then you are on the path eventually loving what you do.

Finding Your “Life Compass”:

Many people after reading this might say, “that’s great Oliver, but I don’t have a compass, and quite frankly I still have no clue what I want to do.” There are a few things you can do to try and some questions you can ask yourself to try and find your compass. Think back to what you enjoyed in high school, as this often tends to be the start of what people’s “career discovery” phase. Think about things that you are generally good at, ask friends and family if you can’t think of anything. If you are still having trouble this is where the exploring phase can work well. But you have to spend time actually trying things, not just reading about them. It can take a while before you develop a true interest in something so don’t give up on something after 1 day of it being challenging or not working out the way you thought. The most important thing, and this is advice I often struggle to follow myself, is to put yourself out there. If you don’t have your compass, you need to be spending time to find the compass. If you have the compass, you need to be spending time to build good habits and a system that will help you “train” in order to become a “professional” at your chosen career path. All of this is hard, all of this will be a huge exercise in failure. But if you work through the challenges, learn from your failures, and defeat the fear of failure (you don’t know till you try) you’ll make great progress towards you overarching goal.

Reframing Failure: Failing is Awesome!

As a side tip from another book, try to reframe failure as being “awesome”, like “hell yeah, that was hard as hell, I just fell flat on my face, I’m ready to get out there and do it again!”. I think the advice of finding what you love as a function of practice, training, and hard work, rather than simply a function of “do what you love” or “do what you’re interested in” is much sounder advice. In simple terms I think people should “do what they are good at, and practice to become an expert.” This advice builds resiliency in children, teaches them to have grit, and to not be afraid of failure (weird how that happens as you get older). I completely understand why many student nowadays are having a hard time unfreezing themselves from paralysis by analysis. They’ve learned to avoid failure at all costs, and especially with the internet and everyone’s lives being online, it can be extremely damaging and unforgiving to fail in public. If you fail a course at school, or do poorly on one test, your chances of not getting into the best university could be lost, so the pressure is high, and the consequences of failure are high as well. Which is the exact opposite approach we should be teaching. It’s good to experiment, it’s good to try new things, it’s good to iterate, and importantly one of the best ways to avoid a future failure when you need to perform, is by failing so many times in private that it’s unreasonable you’ll be unsuccessful (i.e. doing lots of math problems, or making hundreds of cold calls, or lots of songs, or lots of paintings). Fail so much, and become so good, learn from your mistakes, that when you do put your practice to work, even a bad day will still be a good result. We need to be providing more and more opportunities for students to fail in private, and more importantly emphasizing that practice is important in every aspect of life; a career is no exception. I even believe that failing in public can be a great lesson, but I think too much negative feedback when someone is just starting out can be destructive to the motivation to do that thing in the long run, and it can be hard to come back from too much hate about the path you want to pursue. So in the beginning maybe some sheltering from failure is justified. But over time, once they’ve built the failure muscle, and understand that failure is awesome, and decide to just give things a go and focus on constant improvement, the negative feedback becomes easier to deal with as competence grows, and funnily enough, the failures might decrease, at which point I encourage constantly pushing the needle to get better and better. I strongly believe that if we were pushing this kind of advice, rather than “do what you love”, people would be loving what they do a whole lot more, and the generation of directionless young people would have a much easier time finding their direction.

Thanks for reading, I hope that you found this article helpful or interesting. Feel free to email me, I’m always interested in hearing what other people think about these articles. As always,

Keep practicing,

Oliver Foote

Newsletter Email Archive Sent: August 6, 2024:

Newsletter #19: Is “Do What You Love” Good Advice? The US Stock Dip, Toronto July Real Estate Stats

This Weeks Blog Post:

“Do What You Love” is Backwards: Stay Focused, Learn to Fail:

Figuring out what you want to do with your life can be a challenge at the best of times

My take on becoming an expert, and learning to love what you are doing

Pulling ideas from Grit by Angela Duckworth and The Algebra of Wealth by Scott Galloway

I’m actually going to start by talking about the recent dip in the US stock market. I was asked what happened and why there was a sudden drop in prices, the answer seems to be that a bad jobs report came out with the US unemployment rate, in one month from June to July it rose by 0.2 percent to 4.3% y-o-y. The number of unemployed American’s increased by 352,000 in one month. A year ago the unemployment rate was 3.5%.

The trend has been increase unemployment in the US since about February of this year, while Canada’s unemployment rate rose a lot sooner but also affects 10x fewer people. So a big move like this in the US can be viewed by the markets as a somewhat slippery slope for the economy if the trend continues to worsen. This large change was not priced into the market, but now the market is pricing in some larger drops in the unemployment rate. So if this turns out to have been a 1 month anomaly of an event then I expect the markets to recover from their recent dip.

Tiff Macklem, governor of the Bank of Canada has made is clear that if inflation remains at current levels and doesn’t show signs of running away again, he is likely to cut rates again in 2024, and a Reuter’s poll is showing 2 more rate cuts in 2024, which would be a total of a 1% drop in interest rates. Canada is also struggling a bit more than the US with the employment rate, and there have been some signs that employers have been less willing to hire, seasonal student work has been especially hit this year. This is likely going to factor into the decision to bring rates down further in an attempt to avoid a recession (although I’m of the belief that there is a “silent recession” going on).

Toronto Real Estate Market July 2024 Stats Update:

With the heat of the summer and the recent cuts to interest rates by the Bank of Canada the volume of sales in July ticked up over last year. Sales volume has begun to rebound since 2022 when the Bank of Canada was combating inflation and raising rates, sales are up almost 10% compared to July 2022’s figures. Even with the growth in sales volume, buyers continue to benefit from more choice with the number of active listings up 55% to 23,877 over last July. With a better-supplied market, prices, on average, have remained relatively flat compared to the same period last year.

Even with an increase in volume of sales, the average selling price of $1,106,617 represented a small decrease of 1.1% over July 2023. TRREB’s Chief Market Analyst Jason Mercer recently stated that as more buyers take advantage of more affordable mortgage payments in the months ahead, they will benefit from the substantial build-up in inventory. The above average available inventory of homes for sale will initially keep home prices relatively flat. However, as inventory is absorbed, market conditions will tighten in the absence of a large-scale increase in home completions, ultimately leading to a resumption of price growth.

Market Performance as of open Tuesday August 6, 2024:

Canada CPI Inflation June 2024: 2.7% (0.2% Decrease from May 2024) Current BoC Benchmark Interest Rate: 4.50% (0.25% Decrease on July 24, 2024) Unemployment Rate June 2024: 6.4% (0.2% Increase from May 2023)