This idea came back to my mind because I heard in the news that the Toronto Real Estate Board saw a decrease in membership for the first time in 20 years. The real estate business was becoming a lot harder for a lot more people. The number of sales from the peak crazy year 2021 has been cut in half, which means literally half as much to go around. So this post is going to be a bit of an analysis about this problem, as well as talking about which realtors are able to continue doing this over the long term compared to those who are leaving the business. I also want to throw in a bit of my own story here, because I’m learning that being a Realtor is much harder than the successful people make it look.

The Famous # of Sales Chart:

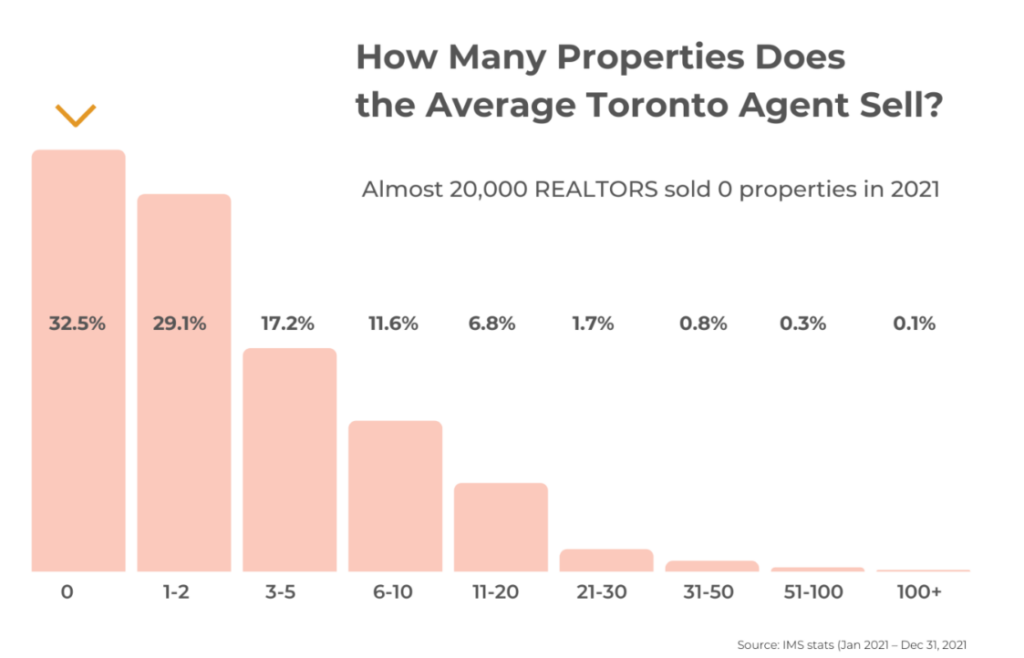

This is a topic that if you’ve ever looked into the real estate industry you’ll know comes up time and time again. I’m going to use the area I work in, Toronto, as the case study, but I’m almost certain if you look anywhere else in Canada or the US you’ll find the exact same thing. Here’s a chart talking about the number of home sales each Realtor made in the Greater Toronto Area in 2021.

In 2021 it was a record year for home sales in Toronto with the Covid vaccine being distributed and the interest rates so low to stimulate the economy. 121,000 sales were recorded, which we can assume for simplicity that each had 2 agents on either side. This means a total of 242,000 transactions were completed.

As the chart helpfully points out 32.5% of realtors made ZERO sales. Which is a TON of Realtors. I’ll get into the numbers a bit later, but doing ZERO sales means that the decision to be a realtor is costing people. From my own lived experience, I’ve averaged around $7,000 in random licensing fees, desk fees at my brokerage, and misc fees, just to stay licensed and run my business. Which quite honestly I do very cheaply compared to the marketing spend of some other Realtors. I know there are cheaper ways to stay licensed than what I’m doing, for example going with discount brokerages. But it would still run me probably around $3,000 a year bare minimum to stay licensed. Which isn’t an insignificant amount of money.

Looking at some more stats. The average home price in the GTA at the time was around 1.2 million dollars. Assuming an average commission of 2% after brokerage splits, fees, and expenses for listing a home and sharing a commission with another agent. The net income on a sale per side would have been around $24,000. In my opinion, this means that you’d need to be making around 3+ sales per year in order to survive in the business, considering all the other fees and targeting the median income of around $60,000. Doing 3 sales and having a net income of $60,000, is a pretty nice deal, but I’ve also learned that it’s not something everyone is capable of doing. As evidenced by the chart, the competition is stiff, and the few winners really take the lions share in this business. The top 10% of realtors do almost all of the business while the other 90% are picking up scraps by comparison. So what makes these top 10% or top 1% so special?

Visibility Trumps Ability:

Going back to the chart for a second, you’ll see that based on my rough math on 3 sales, about 50% of realtors are making barely enough to get by or not getting by at all. So what are they doing? Are half of realtors working part-time? Are they delusional? What’s going on? I think it’s a bit of everything above. Many people who are doing less than 3 sales per year are probably doing it part time, maybe they only sell their own properties, or they just aren’t cut out for the competition. They my also just be unwilling to spend money to market themselves, which as you’ll see below. Is quite an important thing to do.

I think there should be a big disclaimer before people enter the real estate industry that they need to budget around $10,000-20,000/year or more just to dedicate towards a marketing campaign. This might seem like a lot of money to someone just starting out. But I can tell you from what I’ve seen working on a team the amount of time, money, and effort it takes to really take this career seriously. If you aren’t willing to invest either an enormous amount of time or money in marketing, you will likely die a slow painful death in this industry along with the 90% of agents who do less than 10 sales a year.

Most Sellers Sell With The First Agent They Call:

Real estate is an industry of visibility. There have been stats and datapoints showing that most people only know the names of 2 or 3 realtors off the top of their head. When they go to sell their home, most homeowners only interview 1 realtor (per National Association of Realtors in the US). What this means is that you have to be the first Realtor who comes to mind for a homeowner. But most homeowners only sell once per 7 years. So if you want to be doing lots of business, you need to be the first that comes to mind in hundreds, if not thousands of people’s minds. If you are able to accomplish this you’ll likely be one of, if not the only one potential sellers will call to list their house. You can be a complete dunce, an arsehole, rude, etc. BUT, as long as people know your name, and you’re the first one they call. You’ll likely do more than ok in the real estate business.

Selling Agents Rule The Business:

Another important thing to note is that most if not all of the Realtors who are in the top 1% bubble, are primarily selling agents. Listing homes also happens to be one of the only ways that this business is sustainable long-term. The reason is simple to see. In most markets, but especially hot markets, being a listing agent trumps being a buying agent any day of the week. In a market where there is a ton of competition, and say for example there are 15 offers on a property and the sale numbers are going insane. Only 1 of the buyer agents will earn a commission, and the other 14 agents will have to continue to show their clients properties. It may take them 10-20 or more listings until they earn a commission. If the buyers agent is really unlucky or the buyers aren’t very motivated, they might have spent months or years with clients and never make a sale. However, as the selling agent, you’re almost guaranteed to earn a commission from your listing in a hot market. Obviously, some sellers have unrealistic expectations, may be unmotivated, or the house might not sell for various other reasons.

Even in a cold market, as the selling agent, you still have the advantage. You aren’t worried about scheduling appointments, or doing x number of showings per week in order to try and find something your clients like. You make sure to present the property well, take good photos, set a good price, work with your sellers, and wait for other agents to bring you offers and you negotiate for your clients. As a listing agent it’s feasible to have 20 listings up at a time. Buyers agents will show your listings to their buyers, that’s like having an army of people working for you to get the house sold. But once you’ve staged, listed, and marketed the property on all the usual channels, as a Listing Agent it becomes a waiting game, rather than a chasing game, and you can spend your time seeking other listings. Meanwhile, as a buying agent it is almost impossible to show 20 properties in a day and even if your clients do find one that they like, you may get beat out by other buyers or the seller may be unwilling to sell, and you have to keep on keeping on. Being a buying agent simply does not scale beyond a certain point.

What’s holding Agents back?

I’m sure you’ve heard stories of people who enter the business and immediately are making tons of money and tons of sales. How are they doing it? The simple answer is that they are probably much more willing to spend money and take risks than your average realtor. They probably have a pre-existing network of people that already know and trust them and have good relationships with. They’re also probably a competitive person. Lastly, they understand that the name of the game in real estate is selling and put their time and energy into becoming a selling agent not a buying agent. Which is why almost every single real estate billboard you see talks about how “I’ll sell your home in x days!”, or “Our listings sell x% above market average”, or one I really like, “top 10 things to do when selling your home. 1. Call me. I’ll handle the other 9.” All of these Realtors with these big marketing campaigns know that selling is the way to go. Side benefit, you might get a few buyers calling you as well. No reason to turn down business.

Concluding Thoughts:

I think we can surmise that the 50% of agents who aren’t surviving are likely missing one of the key components I mentioned. Likely, they aren’t willing to put in the time or the money that is required to become the top agent that people will think to call when they sell their homes. They probably aren’t thinking long term about the business model and what is sustainable. I think a lot of agents may also be scared of trying to list a home. From experience I know that it can seem like a daunting task to get a home picture ready and staged properly, you’ll likely have to put in some money up front to do it the right way as well, with the possibility you don’t see a penny of that money ever again. But it’s important to realize that if you’re unwilling to learn how to be a listing agent, you should probably exit stage left before you go broke. You’re competing for peanuts with the 90%, not the big prizes with the top 10%.

That’s going to do it for now, this post is a bit more brief than usual. I originally wanted to discuss a bit more about my own finances. TL;DR: I’ve discovered that between owning a car and being a realtor I’m burning around $14,500 per year. I’m not sure how relevant the discussion about my personal life goals and finances would be to this blog. But I’ll just leave you with this thought. Owning a car is not a good financial decision, unless it makes you much more money than it costs you. Being a realtor who does less than 3 sales a year and doesn’t have a business plan that leads to being a listing agent is also not a good financial decision. In order to be a Realtor you almost certainly need a car. Meaning that owning a car solely to be a Realtor, can be a VERY bad financial decision if you’re not serious. Thanks for reading, hope you found it interesting or useful. As always.

Subheading: The blog this week is discussing: “Why are most Realtors broke?” You may have heard about why some Realtors perform better than others. There are some fundamental reasons, and I discuss what those are in the post. Also BoC cut rates by 0.25bps! Will this help buyers? Certainly should.

This Weeks Blog Post:

Why Are Most Realtors Broke?:

The question, should you list homes or should you help buyers?

Why some Realtors do better and outcompete others.

The crazy cost of Realtor fees, just for the privilege of being an agent.

The Bank of Canada cut interest rates on Wednesday Jan 29th. This means that the overnight lending rate now sits at 3%. For us normies, that means that the prime lending rate at banks is now at 5.2%. With some banks offering prime – 0.3% on 5 year variable rate mortgages. That puts the mortgage at 4.9%. The 5 year bond yield, which determines fixed rate mortgages, is sitting at 2.8%, which is nearing a 52-week low. You’ll likely start to see 5-year fixed rate mortgage below 4.5%, with some as low as 4.2%. If yields drop enough to the point where we start to see a leading 3 on mortgage interest rates, I believe this will be a psychological breaking point and people will return to the market in droves. Potentially just in time for the seasonally hotter Spring market. If yields continue to fluctuate the way they have been, or the tariff war heats up with the US. It is possible that yields go up, the BoC has suggested they may even have to raise rates again. This would mean that the market would be unlikely to see a significant rebound this year.

A new AI model just hit the Interweb, DeepSeek AI. This AI large language model (LLM) came out of nowhere from a Chinese company. They were able to train the model for a fraction of the cost of ChatGPT, while delivering comparable performance, and also being Open Source (free). This news caused the market to fall somewhat on Monday. NVIDIA, the leading chip maker supplying OpenAI (and all the other big tech firms) with very expensive AI hardware to run their learning models on, saw a dip that caused NVIDIA to lose $600 Billion dollars in market valuation in one day. The following day it recovered around half that loss. Another model built by this firm was able to compete and outperform with one of the best image generation models currently available.

Stock Market Performance as of Wednesday Jan 29, 2025:

S&P 500: 6,039.31 (+2.91% YTD)

NASDAQ: 19,632.32 (+1.82% YTD)

S&P/TSX Composite: 25,473.30 (+2.31% YTD)

Macroeconomics Statistics:

Canada’s CPI Inflation Dec 2024: 1.8% (0.1% Decrease from Nov 2024)

Current BoC Benchmark Interest Rate: 3.00% (0.25% Decrease on Jan 29, 2025)

Unemployment Rate Dec 2024: 6.7% (0.1% Decrease from Nov 2024)

Greater Toronto Area (GTA) Real Estate Stats – December 2024:

November 2024 Average Selling Price All Home Types: $1,067,186

Y-o-Y (comparing Decembers) % Change in Average Selling Price: -1.6%

YTD Number of MLS Sales: 67,610

YTD % Change in MLS Sales (compared to this time last year): +2.5%

Y-o-Y (comparing Decembers) % Change in MLS Sales: -1.8%

Number of MLS Sales in December: 3,359

Y-o-Y (comparing Decembers) % Change in Active Listings: +48.5%

Number of Active Listings in December: 15,393

Inventory Available: 4.58 Months (Increase from 3.71 Months in November 2024)

This was a very interesting question I got asked recently and it really got me thinking. So much so, that I decided it warranted an entire article to address it. The question is: when can you stop saving money and be confident that you’ll retire securely? In other words, when is the nest egg that you’ve squirreled away big enough that you’ll be able to loosen your wallet and start spending all of your income. This sentence probably made prudent frugal savers panic a little, trust me I know, I’m one of them. For the sake of argument, let’s do the thought experiment. When will the amount of money you saved be able to grow enough to allow you to retire by your planned retirement date, without saving a penny more. When will this small nest egg of money compensate for a lack of savings? Lets find out.

Psychology of Money

This question fascinated me because it also bridges into another domain related to the psychology of money. I think there’s almost a secondary underlying question here, when is enough, enough? When can you relax a little and spend a bit more on life, knowing that one day you won’t be here, or that one day you won’t be able to work the same way you can today? Well, let’s do some math, make some assumptions (which are always wrong if your time horizon is large enough), and see what we can magic our way into existence.

Step 1: Understanding Your Annual Expenses in Retirement:

There are a few ways to approach this problem. But they all require understanding what your monthly expenses are, and what you plan for them to be when you retire; plus a little safety cushion since inflation can be somewhat unpredictable. Lets take myself for example. I currently live in a 1 bedroom apartment in Toronto, I’m paying $1200 a month in rent, with all the other random bits a bobs of expenses, having a car, travelling between two cities for work, student loans, eating, gym membership, stupid financial mistakes. I’m burning around $3000 a month. I can see how it’s feasible that in the somewhat near term future, I move into a new house and my expenses jump again. Let’s say that 5 years from now I’ll have doubled my expenses due to a mortgage and lifestyle inflation etc. Let’s say another 5 years after that I’ll be spending close to $10,000 a month raising a child and all the expenses that come along with that. After which point let’s say that the expenses stay somewhat steady.

Now let’s think about retirement. In retirement, I’d probably want to travel a bit. At which point my mortgage should be paid off and I won’t be raising kids anymore (probably). So if I aim for around $12,000 a month in spending or $144,000 per year in expenses, that gives me a good goal to reach for. I will say, from the relatively moderate amount of money I’m making and spending now, it seems a bit crazy to me that I might some day be spending anywhere near $12,000 a month, but things do get more expensive with time, lifestyle inflation is a real thing, and just based on recent history I think taxes will be higher 40 years from now than they are today which will eat away a bit at the budget. Someone come back to this post in 40 years to fact check me on that.

Now that we have come up with these hypothetical numbers, and assume that we’ll be spending $144,000 a year in 2065, we can reverse engineer a bunch of ways to get our income up to that level. This is the point at which the potential pathways really start to branch off and the old saying “there’s a million ways to make a million bucks” starts to involve itself. But instead of a million methods, lets narrow it down to 3 or 4. Namely: Stocks and Dividends, Real Estate, & Business Income.

Method 1: Stocks and Dividends:

Bank Stocks:

One way to “retire” or “stop saving” is to have enough money saved and invested in dividend paying stocks that all of your annual expenses are covered. For example, a common method of doing this here in Canada is through the big 5 bank stocks and insurance companies. They pay out around 4-6%/year depending on the bank and the time at which you bought shares. Some of these businesses have over 100 years history of paying their dividend so you can rest pretty well assured that you have a decent shot of seeing that payment into old age. Canada also tends to have a better history than the US of regulating it’s banks for stability. But if you are worried about bank collapses and the like, it may still be prudent to diversify among banks and not put all your eggs in one basket or even one country. 2008 proved that you can in fact mess up being a bank, and it can happen in multiple countries.

Oil and Gas:

Oil and gas stocks also have a great history of paying very good dividends anywhere from 7-12% depending on the stock. Many oil and gas companies also have the claim to fame of being around for over 50 years some approaching 100 years. Nowadays, a lot of oil and gas companies are investing in green energy, but I think the lions share of their income continues to come from oil. I would consider oil a slightly higher risk investment than banks, but I also really don’t see these companies going anywhere anytime soon. You also have to invest in line with your morals and there are a lot of people who do not invest in oil and gas simply because it goes against their beliefs and that’s perfectly fine. You have to make a decision on what to invest in. However, to counter the green argument, you may need less money invested in oil and gas in order to “retire” and stop saving, so the trade off may be worth it to you.

Now that we have 2 industries, lets do some math. Assuming that we’re all in on one industry or the other. How much money you’d need saved up in order for dividends to fund your life in retirement? If we take a 5% dividend rate for banking, we can simply divide our annual expected expenditures of $144,000 by 5%. Which results in a portfolio value of $2,880,000. Just to be safe lets round up and call it $3 million. For oil and gas if we assume an 8% dividend, you’d need a portfolio of $1,800,000. I’m going to stick with banks simply because I think it’s a safer investment and the larger portfolio leaves more room for error. If you recall our original framing, we will need the $3 million portfolio when we plan to retire in 2065. That doesn’t mean we just save money every day a stick it into a savings account until we hit $3 million. Naturally, you’d want to invest the money along the way so that it’s working for you while you’re working to earn money.

The Power of Compounding:

This is where an important concept called compound interest comes into play. We have 40 years of investment to play with here. So lets play a fun game and determine what will happen if you have x dollars today, and you didn’t save a penny more, what that money would become in 40 years. (This will also be useful for future examples).

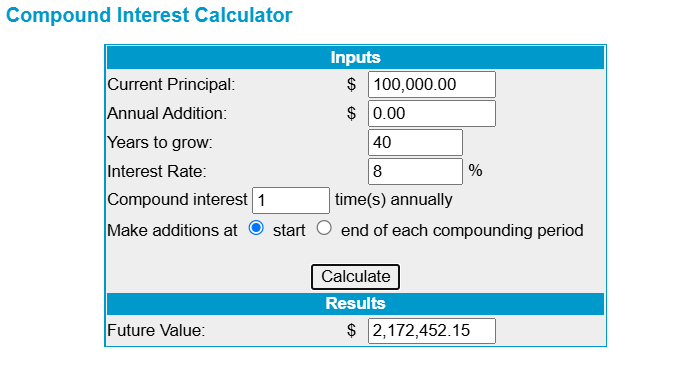

Compounding: $100,000 for 40 years @ 8%:

I pulled out the trusty old compound interest calculator for this example. Again, some assumptions have to be made. I’ve used a growth rate of 8% as that is what is commonly quoted as a sustainable long-term interest rate for your money invested in the US S&P 500. We have to use some assumptions, so this is what I’ll be using. If you want to be more conservative you can adjust the compounding rate lower to account for stupid mistakes or underperformance of stocks. For the sake of these examples I’ll stick with 8%. You can see that if we start with $100,000 at age 25, using our assumptions, we’ll be 65 with $2,172,000. Not too shabby.

The truly crazy thing about compound interest is that the real explosive growth is at the end, it will take 30 years for the $100,000 to grow to $1,000,000 as seen in the last column of this chart.

However, the following 10 short years, the money grows MORE than $1,000,000 as seen below:

Our final number is $2,172,000. This is still about $800,000 short of our target of $3,000,000. But it’s pretty damn good for not saving a penny more for 40 years.

Something that makes this EVEN crazier is thinking about what might happen if you START with $1,000,000 and invest it this way. In 10 years, you’ll have made over $1,000,000. In 40 years, it gets truly INSANE, as you’ll see in the third example below. There is REALLY something to be said for saving and investing AS SOON AS POSSIBLE. Time and patience are the true money makers.

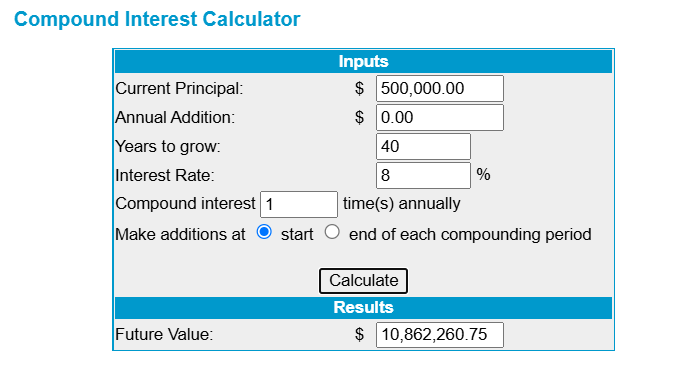

Compounding: $500,000 for 40 years @ 8%:

So let’s just jump into a whole other world, and say that we somehow accumulate $500,000 at age 25. Well, if we just invest it and do nothing more, it can become almost $11,000,000 in 40 years. For most people that’s a “holy s***” amount of money. Obviously, the reality of having worked and saved $500,000 by 25 years old is not likely to say the least. But, there are a handful of people out there who have secured their future well beyond what they’ll need at the ripe age of 25.

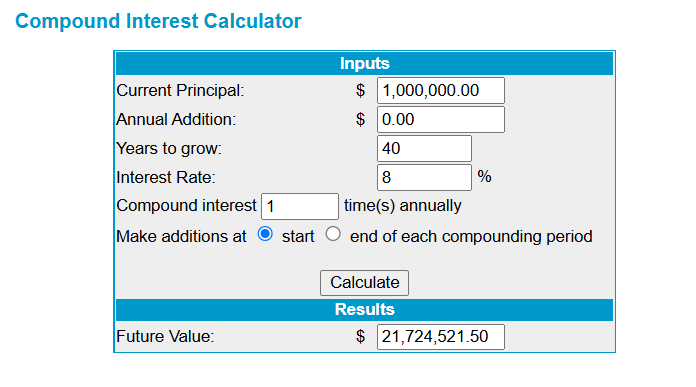

Compounding: $1,000,000 for 40 years @ 8%:

This is where the true insanity begins. At this point we’re pretty far diverged from the original question and from most people’s reality. But I find this stuff fascinating so bear with me. If you recall from above, $1 million dollars grows to about $2 million in 10 years using our assumptions. If you give it another 30 years. According to this VERY linear calculator (read: no likely). You could end up with over $21 million dollars by age 65. Crazy. Absolutely wild to most people. Ok enough daydreaming, lets get back to reality. How much money would I actually need to save to get my $2,880,000 portfolio number.

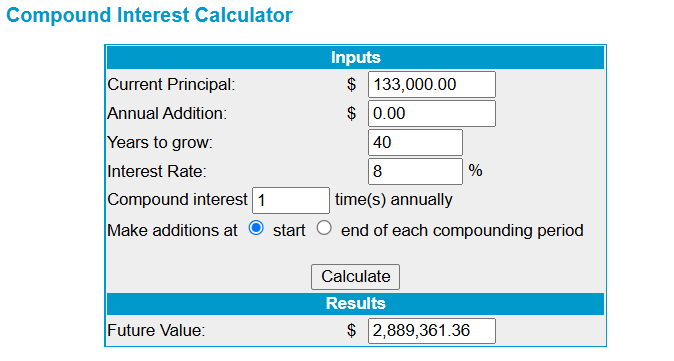

Compounding $133,000 for 40 years @ 8%:

I found that quite a close estimate to get to the retirement number is $133,000. This is still a lot of money for a 25 year old to have squirreled away, but not an entirely farfetched amount of money to have at that age. Do I know any 25 year old’s (soon to be part of the gang) with $133,000? I can’t say that I do, and even if I did I can’t say that they’d want me to know. But considering that it takes 4 years to get a university education and you could start earning a decent salary by 22 or 23, if you live at home for a couple of years and don’t spend a dime, yeah you could have over $100,000 saved within a few years. The name of the game is work your butt off, keep your expenses low, live at home as long as possible, and profit. The hard part will be not touching the money for the next 40 years.

Bringing this example to a conclusion. As seen above, if our dividend stocks are paying out 5% per year and our spending will be $144,000 a year, we’d need to have about $2,880,000 saved by 65. This can be achieved by starting with $133,000 at the age of 25 and investing it in the S&P 500 for 40 years, in theory. The gargantuan amount of assumptions here probably has statisticians rolling in their graves. But what can you do. If this example isn’t completely relevant to you then you can definitely do this yourself and adjust to your scenario start at a different age, change the dollar amounts etc. However, fair warning, the older you begin investing the larger the starting number has to be. I had a short story here about how investing young set me up for success, was a bit too much of a diversion, that’ll likely be my next post. For now onto method 2.

Method 2: Real Estate:

How Many Rentals?

Many people who have done well in life usually have some amount of involvement in real estate. So I’m going to approach this from the angle of the monthly rental income amount that you’d need in order to retire on rent payments. Naturally, to buy real estate you need some starting capital for the down payment, and a good income to qualify for the mortgage. So the hurdles are a bit higher. The nice thing with this example is that we can stretch the timeline. Most mortgages are 25 years in Canada.

Shorter Timeline

This means that even if we start investing at age 35-40, we can retire 25 years later with paid off homes that cash flow a good amount of money every month. You can also make the argument if you’re a younger person that, “hey, if you’re telling me there’s a way to hit my number in 25 years, why should I do the other method?” Good question, and good thinking. Depending on when/where you are looking for a house, you may find that even the $150,000 you have saved at 25 isn’t enough for a down payment on the house that you would like to invest in. You may also be in the strange position of not having a high enough income to qualify for the mortgage, but in theory having a large enough down payment. This might mean that you have to progress in your career a bit more before buying, or team up with someone else, to begin investing in real estate. I have written a couple blog posts about real estate investing so check those out too for more tips and tricks.

Historical Rents Growth

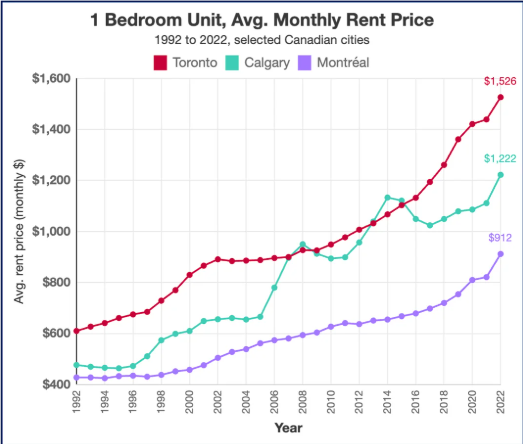

So let’s see what it would take to generate $12,000 a month in rental income (profit) from our rental properties. First thing that we should do is find out what the average rental growth rate has been historically in the city that we want to invest in. I’m going to take Toronto as my example. I found this handy chart:

Which shows the average monthly rental price of a 1 bedroom unit in Toronto. In 30 years it went from $600 to $1525. So if we divide the two 1525/600 = 2.5417, that’s about a 2.5x increase in rent prices in 30 years. I think this is a fair assumption to make and may even be on the more conservative side..

Target Rent Amount

So we can take our target number of 12000/2.5 = 4800. So we need a portfolio of properties that will be paying $4800 of rent today, in order to retire on $12,000 of rent in 30 years or so. I’m a bit worried about the state of rent growth in Toronto to be honest at the moment, so I’m going to target $6000 of rent today. It’s important to remember that we don’t really care if these houses are making a profit while we are paying down the mortgage, re-investment is fine. Once the mortgage is paid off, all of the money will go straight to you instead of the bank, which is the goal at the end of the day.

Example Property

Searching through recently sold listings on the MLS I was able to find a property that almost perfectly fits the bill. It’s a 2 unit property in the Annex neighborhood of Toronto (one of my favourites). Close to downtown, U of T, Yorkville, and hundreds of restaurants. It was sold in August of 2024 for $1,250,000. One unit was comprised of the 2nd and 3rd floors and this was listed for rent at 4800 after closing, and the main floor unit was listed for rent at 2400. Nowadays, rental discounts are quite common, but even if both units rented out for just under asking, they would have almost exactly $6000 in rental income, which hits our target.

Mortgage and Carrying Costs

The mortgage on the house would have been around $6200 based on a 5.5% fixed rate at the time of purchase assuming a 20% down payment, so it would likely cost around $1000 a month to carry the home factoring in all expenses and property taxes etc. or around $12,000 a year to carry. Believe it or not that’s not horrible for a big city. Especially considering that this type of housing has historically appreciated 6.7% over a long time horizon.

Closing Costs and Rates

You also have to factor in the fact that interest rates have come down since August 2024, so if you took a variable or open mortgage at the time you could wait until rates get a bit better and then lock in a fixed rate mortgage and get even closer to breakeven on your expenses. Let’s talk closing costs. The 20% down payment would be $250,000, land transfer tax in Toronto would be around $40,000 since you get hit with a double tax. Then misc closing fees probably add another $5000, then just throw in $5000 in repairs and unexpected costs and you need to come up with around $300,000 to close on this house.

100% of Zero

$300,000 at 25 as we’re assuming in this example, is not something that most 25 year old’s will have. However, if you potentially pool in with another person, whether that’s a spouse, a parent, or a business partner or two, you might be able to come up with the cash to do something like this. Yes you won’t get 100% of the benefit for yourself. But if you NEVER do something like this you’ll GUARANTEE that you’ll get ZERO benefit for yourself. As the old saying goes 100% of nothing is still nothing. Get involved, and make a plan with the people you buy with. Will it be a lifetime buy and hold situation, will it be a fix and flip, will it be a hold for a couple years while we wait for the market to recover then sell when things are looking up and move the proceeds into something different situation. There are lots of options and ways to get involved, and that’s the most important part, you can’t win if you’re not playing.

Qualifying Income

The other side that may complicate your grand strategy and push your timeline to purchase real estate is income. I know personally, I do not have anywhere near the income needed to qualify for a home that costs over $1,000,000. On top of that I’m self-employed which means I need a history of making decent money, and will probably have to go to a “B lender” to get my mortgage (and pay them a 1% finders fee). But if I team up with people who have a regular income, we may be able to work something out with a traditional lender and avoid the fee. The important part is figuring out what the collective income required will be with the people you want to purchase the real estate with, or what your personal income needs to be to do so.

Debt Service Ratios

You can also lower the income requirement by increasing the down payment. There are many mortgage affordability calculators that you can use to calculate what the income number will be. The things that factor into the equation are other debts that you have, property tax, heating costs, and half of your monthly condo fees (if a condo). Any monthly payments will bring down the loan you can carry. In banker terms your debts increase your gross debt service ratio (or GDS). Assuming around a 5.5% fixed mortgage rate with minimal other debts. You’d need approximately $220,000 before tax income to qualify for the property. So you can see how income becomes one of the largest hurdles, and why teaming up may be an inevitable route you have to go down.

Partnership

Let’s say that you do team up with two friends, for the sake of this example. The partnerships long-term plan is to own and rent 3 similar properties and pay off the mortgages on all of them in 25 years. Let’s also say for the sake of argument, you’re able to purchase your first property at 25 years old and then at a pace of 1 property every 3 years thereafter. So by 31 you have 33% ownership in 3 properties that are generating around $18,000 in rental income for the group or about $6000 per person BEFORE expenses. Collectively the properties are probably costing you around $1000 a month to carry for the first 5 years. After which you renew into a lower interest rate since rates are coming down (for now).

Final Results & Going Further

In approximately 19 years after turning 31 you’d be generating (remembering our doubling of rent rule), around $4000 a month in rent to yourself, then 6 years later you’d hit your retirement number of $12,000 a month assuming everything goes according to plan. Maybe you’re generating a bit more, and the property maintenance doesn’t have to come out of your pocket. In the end you’d be 56 years old and living off your rental investments. That’s almost 10 years earlier than the stock market example. If you really max out this example, and you try to do bigger and better things. For example, you become a partial investor in many more properties, or take a completely different approach like fixing and flipping in order to speed up your mortgage payments. You can make a TON of progress very quickly and get to your retirement number even faster. But that all depends on your willingness to participate and execute on your plan and find people who can help enable that plan alongside you, or move to a market where it may be possible to do it yourself. Let’s move on to our final scenario.

Method 3: Business Income:

Now that we’ve talked about what I would consider to be the most common ways that people are able to build wealth. Let’s talk about something that is a bit more challenging but can still yield the results that you’re looking for and more. I’d probably consider this to be the most complicated of the options, but it can also be the most lucrative, consistent, and the one that you personally have the most influence and control over. That would be building and owning a business that brings in income for you, without your intervention. The last part of that sentence is key, and also extremely challenging to accomplish.

The “Easy” Method

The internet would have you believe that starting a business is the easiest way to become a millionaire and retire. After being involved in various types of businesses, and speaking to business owners who are working their butts off and cursing their decisions, I can’t disagree more. This is the hard way. The “easy” way (in my opinion, there is no “easy” way, just get used to doing hard things instead) is get a good job, spend less than you make, and ideally save the bulk of your income. Invest it for a long time, then sit back, relax, and watch your nest egg grow. Getting a business up and running successfully on the other hand is a whole other can of worms, and getting a business to run successfully “on it’s own”, is an even bigger ask. But let’s just play with the idea a bit and see what we might be able to come up with.

Creative Industries:

There are various types of “businesses” that could pay you a passive income of sorts, so I’m going to try to bunch categories together. First is creative industries, this involves things like creating music, being an author or publisher, making YouTube videos online, creating and selling classes, even creating a software program or video game. The common thread among these, is that you create something once, and it can be consumed an infinite (or close to infinite) amount of times and you get paid each time that it is consumed. Obviously if you don’t market it and no one knows about it, then you won’t get a single sale. But if you are wiling to put some time and money into marketing these can be quite lucrative.

Not all of these are equal in terms of how much they will pay out, but software is especially lucrative because it can frequently be a higher ticket item, and once the initial R&D costs are paid down, it’s all profit afterwards. Sometimes there are recurring maintenance costs, but these tend to be quite low compared to the income if a product is successful. The problem with these types of industries is largely relevance and marketing, in theory, you can be a one hit wonder that sells and sells and sells until the end of time with no further inputs. But in practice you do have to maintain, upkeep, renew, and refresh as a bare minimum to keep your sales going. But the small amount of upkeep of brand image or what have you can be well worth the rewards.

Franchising:

The next category of business that you might consider going this route is franchising. This can be both from the angle of being the franchisee or the franchisor. This type of model is frequently associated with a fast food business, restaurant, or service business of some kind. Popular examples are Starbucks, McDonalds, 1-800-Got-Junk, etc. The franchisors in these businesses have built up the brand and then systematized it until it is easily replicable, then they can sell business units to franchisee’s who buy in for a certain fee and then operate the business based on the manual created by the franchisor. The franchisor is frequently responsible for the marketing and maintenance of the brand image and keeping things fresh, while the individual franchisees are responsible for operating the business as dictated by the franchisor, sometimes with some flexibility. In exchange for providing a solid brand, marketing, and a “business in a box” to the franchisee, they generally pay the franchisor a royalty fee on all the revenue that the business generates and get to keep the remaining profit after expenses.

The Franchisor

I believe that of the two, being a franchisor is probably the stronger position to hold. If you are the person who builds up the business, the brand, and are selling business units, it is possible to see how all the things you do can be delegated. You hire a board of directors, you get a strong marketing department in place, you hire a business development team to keep your franchisees going and selling new franchises, and you can step away from the top level business. However, this opportunity is also available to the individual franchisees.

The Franchisee

If the franchise owners become adept at managing their business, running their teams and their schedules, there is real opportunity to also step away from the business and put a manager in their place and then replicate this strategy a few times. The big limiting factor in these types of businesses becomes people management and turnover. Managing multiple franchises essentially just becomes an exercise in managing people, so you either need to be really good at doing it yourself, or be willing to shell out the money to hire someone else who is. Being in a people management business is not for everyone, and can be quite time consuming. Some people may prefer the creative industries route simply because managing people is a lot of headache and overhead.

Professional Businesses/Partnerships:

This type of business will deal with things like, doctors, lawyers, engineers, accountants etc. The nice thing about these businesses is that you can set up a practice, build up a client base, and then train someone to take it over for you once you are ready to retire. If you really want to be able to set this up properly you could do it as a partnership and that way if you retire at some point there will be someone else there who may be able to oversee things while you try to find someone else to take your place. The challenge with this type of business is finding a way to transfer over your database of clients to someone on your team and making sure that they treat the relationships you’ve built with all these people the right way.

A Book of Business

Professional business can be hard to sell, but you may be able to sell a book of clients or a database to someone else. I’ve heard in the world of real estate, I believe this may have just been a stolen idea from the world of accounting and law partnerships. But sometimes what real estate agents do is they will sell their “database” of clients to another agent. For example, an older agent that wants to sell their database may sign an agreement with a younger agent for their book of business. Then they create a sort of sliding scale of referral fees for any income that results from this old agents clients.

Buying a Database

For example in the first year any of these clients who the younger agent does a deal with would split the funds with that older agent 50/50. Then each year after that the younger agent gets 10% more of the deals until it hits 90%, then the older agent get 10% in perpetuity, or until a certain number of years has passed, or maybe even until they pass. This is an interesting way to set things up since the incentives are there for both agents. Ideally these clients are transitioned over to the new agent gradually. The new agent may even use some of the old agents branding and marketing style to keep it consistent for the older clients. The old agent may pop in from time to time.

Each year that passes the new agent is somewhat able to grow into the role and earn more. But the hard part, finding clients, is done, and both agents benefit. The older agent is able to retire and get paid out a few referral fees here and there, and the young agent is able to skip ahead a few years and work with a database of well nurtured clients. Maybe there’s even a “sale price” for transferring leadership of the database to the other agent. There’s a variety of ways to set up something like this, but the important thing is that the database of clients doesn’t go to waste and get scooped up by competitors. The person retiring is able to continue to benefit from all the work they did, even if it’s a small amount, and someone new is able to get a jump start on their career. Win-Win.

Other Industries:

There are a ton of other types of businesses and industries that you could involve yourself in, but regardless of what business or industry it is, if you ever want to be an absentee owner of a successful and well oiled business. You will one way or another need rock solid systems and practices in place that allow the machine to run without your inputs. The biggest and most important thing are systems, guidelines, and people who can properly interpret those systems and guidelines and even improve them. This is the dream scenario and requires some amount of letting go of control. Which can be a challenge in and of itself because the people who tend to get to such an esteemed business position usually did so through sheer power of will and force of their personality. Which can very often correlate with having a bit of an ego. Getting that same type of personality to step down from the pedestal they’ve created for themselves and relinquish control, even if there’s no longer any need for them to be captain of the ship, may never happen.

Business Method Final Thoughts

So to answer the question of the post with my final set of examples. In a business, when would you be able to stop saving money? Well if you’re the owner and you’re no longer running the business, you technically just need to be generating enough profit from the business, for it to cover your living expenses. You technically don’t need to save a penny for retirement in this scenario (although I wouldn’t advise that route) if you’re confident that your business will perpetually generate your $12,000 a month. The cool thing about a business is that if you are the type of person to take on a high risk and dump everything back into a business that is clearly beginning to do quite well, you’ll often be rewarded quite well for doing so and this may be the fastest way of the three methods to hit your “no need to save” number. However, businesses undergo cycles so you’d probably be well advised to do some combination of the above 3 things in order to hedge your bets and diversify once you are in a position to do so. But if the hypothetical is exclusively based on the bare minimum amount of money you’d need to save, this scenario can technically be as low as zero.

Concluding Thoughts:

This was a bit of a longer post, in fact so long I spent about a week putting all my thoughts together and made my whole email newsletter a week late. I actually had to cut out a few ideas because the post was really getting a bit out of hand. But I found writing this thought experiment quite interesting. It was a cool way to synthesize the various paths that you can take to become an above average success. It seems to me that most people who are quite successful are almost always doing a combination of all three of the main points that I made, not just one. But at the same time, they usually have a main thing that is bringing in the bulk of their money and the other’s are slowly but surely growing in the background. There is something to be said for really focusing your energy on one thing at a time and putting everything you’ve got into it, before moving that energy around to other projects. Focusing and doing hard things every day for a long time are what yield real results. Thank you for reading and as always.

There have been a lot of interesting developments happening in Canada related to employment that I think are worth discussing. I’m going to explain why Canada has one of the highest youth unemployment rates it has ever seen, why Canada’s GDP growth has actually been a negative for citizens, and how politics are influencing this issue and what people in power are starting to do about it.

Toronto and Ontario Lag Behind Canada:

The first topic I wanted to touch on is unemployment in Canada and more specifically in Ontario and Toronto where I now live. The unemployment rate in Toronto in November 2024 was sitting at 8.2% which is higher than Hamilton (6.7%), Kingston (5.8%), Ottawa (6.1%), St. Catherine’s (6.6%), and almost every other major city in Ontario except Windsor (8.5%). Toronto’s unemployment rate is comparable to Northern Ontario where work is notoriously hard to find (8.4%). The overall unemployment rate in Ontario was 7.2% which is higher than the national rate of 6.8%. Why is Ontario doing worse than the country as a whole and why is Toronto doing worse than the rest of the province? Let’s find out.

Overshooting Immigration Targets:

Unemployment is the symptom, not the cause. In order to find the cause we need to understand how unemployment works in the first place, and this is generally just a case of supply and demand. But there are other factors at play, like interest rates, immigration and migration, investment etc. As we have all been made aware by now, Canada overshot it’s immigration and migration numbers by a significant amount in the past couple years and the government is beginning to try and put more restrictions on people coming into the country. Generally speaking, Canada has always been friendly to immigration, especially people who are highly skilled workers and are able to contribute positively or fill needs in our economy. It has been stated many times over that the only way for Canada to maintain it’s pension plans and continue growing GDP and productivity is through immigration. If immigration is such a good thing, why have we decided to cut it down? Well part of the reason is that we have nowhere to put people, housing has become such a large issue and pain point, and renting or buying almost anywhere in the country is becoming extremely unaffordable. People will come here, and expect to find a reasonable home and realize that a huge portion of their paycheque is going towards their rent or mortgage. This doesn’t explain unemployment, but it does help explain some issues we have with our economy as a whole.

Highest Household Debt in G7 Curbs Spending:

Another factor in our problematic economy is that Canada has the highest household debt to income ratio in the G7. Meaning that people in Canada are extremely overleveraged on their homes and rent payments. This affects the economy in ways that people may not understand. Traditionally the people who spend the most money tend to be middle class, and spending money is what stimulates the economy and leads to growth and expansion. What has happened over the past few years with the skyrocketing costs of housing, the expensive mortgages that people are renewing into, and general high inflation. Is that people do not have excess money to spend, and consumer confidence is quite low.

Employers Pull Back Investment:

If people are not spending, there is no reason for companies to make investments in their workforces and R&D new products when there is no demand for those things, and in many cases shrinking demand. We now find ourselves in a situation where our GDP per capita (per person) has actually gone down at the fastest rate in the G7. This is a much more accurate measure of quality-of-life changes, as compared to overall GDP growth. Part of the reason per capita is down is because we’ve let in so many people (over a million in 1 year). The overall GDP has gone up compared to a year ago, but per person has gone down. Without all these extra people boosting our numbers we’d be in a technical recession. The way that falling GDP per capita manifests in people’s real lives is the realization that their money doesn’t go as far as it once did and struggling to afford and adjust to fewer things, fewer luxuries, fewer benefits that come with a growing economy. Life has become more difficult and paying bills has become more challenging in the past couple years for the grand majority of Canadians. The average money that Canada produces, per person in the country, has gone down, there is literally less to go around. But the economic headlines don’t usually focus on GDP per capita, they focus on GDP and proudly promote the fact that our economy is (technically) growing.

Newcomer Credentials Not Recognized:

Because of all these factors: high interest rates, high levels of household debt, low business investment, declining GDP per capita, and millions of people coming to Canada, we are suffering an unemployment problem that is getting progressively worse. These problems are also making it even more challenging for all the people and students who come here. I don’t believe that people should expect handouts, but by the same token I’m not sure that it’s fair that we are telling people to come here, and then they’re met with the reality that there’s just no work for them or their credentials aren’t recognized or a million other hurdles are put in their way to succeed. Work is becoming harder and harder to find due to the above, this leads to strains on public services, food banks, and more. By allowing the sheer number of people to come into the country that we did, we are effectively draining our own resources at breakneck speed. Stack on top of this our housing construction issue which is a whole other topic for a whole other blog, and we’re just squeezing people for everything they have. High cost of housing, poor employment, the picture is bleak. A lot of the economic factors I’ve mentioned are leading to the cost of home construction to become un-feasible for builders, and this will lead to a renewed shortage of housing about 3-5 years from now, which is really not what we need added to the pile of problems.

Historically High Youth Unemployment:

Let’s discuss youth unemployment, I’ve been reading some scary things about the 15-24 age group. The core age group 25-54 is currently experiencing above long run average employment levels, the youth age group is not faring nearly as well. As of last year, employment was at somewhat normal levels for Ontario youth, hovering around 11%. But in the latter half of 2024 it has jumped to around 17% and is getting worse. This is problematic because getting a job is important to development for a lot of young people. Your first crappy customer service job motivates you to find a better job, internships lead to future full time roles, and you learn important life skills and how to work with others. These employment numbers getting worse are not only bad right now, but will be bad for the future workforce, youth unemployment is a crisis. France has declared youth unemployment a national crisis, and their numbers are better than ours, what does that say about us? These numbers are also directly impacting a lot of university graduates because it points to the fact that companies are hiring fewer and fewer new grads in an already extremely challenging environment to find work.

University Graduates Struggling to Find Work, Hiring Freezes:

This data backs up what I’ve been hearing anecdotally. I graduated from Engineering in 2023 and I’ve been talking to others who graduated from school around the same time I did. I’ve heard stories of people searching for work for over 7 months to a year and a half AFTER graduation to find work (many still looking). A client of mine that I spoke to a month ago who works for a materials engineering company is currently in a hiring freeze and knows of many other companies who are doing the same. This is as of November 2024. Every engineering graduate I’ve recently spoken to agrees with me when I make the comment, “I wasn’t aware when I started school, that part of the gig would be moving to the US.” Not just to find a job that pays well, but to find any job AT ALL! You suffer through years of engineering just to continue to suffer for another year or more to find a Canadian engineering job, it’s extremely disheartening and I don’t blame people for feeling disenfranchised with Canada or their expensive educations because of it. I can think of a greater number of people from my engineering cohort who are working in the US than those who are working in Canada. The ones who are working in Canada are only doing so because they are international students and have no other choice (or worked their butts off applying), but would much prefer work in the US, and likely will once they are Canadian citizens. I don’t know how else to say this, but we simply don’t have enough jobs in Canada and Ontario to keep people from leaving, and the US benefits from all these people we’ve spent (partial) taxpayer money educating.

Employers Hiring for Experience:

Another relevant point here is that as companies are cutting costs, tightening their belts, and possibly laying off highly qualified workers, why bother hiring a new grad you have to train from scratch where there is a pool of much more experienced, more qualified people for you to choose from. This contributes to the bleak outlook for youth employment. The numbers back this up because employment of core workers is steady and rising, while it is falling for youth. Diverging a bit from the data again, I read recently a comment from a Canadian online forum that you used to be able to just walk into pretty much any retail store and ask for a job and you’d be hired in a jiffy. But even these basic jobs are much harder to come by and staffed frequently by overqualified workers, or workers who aren’t getting paid properly and are becoming harder to find.

Part-Time Work Replacing Full-Time Work:

Another concerning fact is that we are losing full-time jobs almost at the same rate that we are gaining part-time jobs. Our employment situation is actually much worse than the numbers make it seem, full-time jobs are being replaced by part time-jobs and gig work. This is a problem and underscores that quality of life has likely declined for a significant portion of the population. Full-time stable employment is becoming a thing of the past for many people and they are replacing it with one or more part-time jobs. Along the same vein is underemployment, Canada is notorious for this. Everyone has a story of when they discovered that their Uber driver was a doctor in their home country. I don’t have any issue with doctors having to go through recertification and a couple years of training to get up to speed on how we do things here. But there are no spots available for them in residency programs and yet we have a huge shortage of family doctors! What are we doing here?

“98% of Graduates Are Employed”… at McDonalds:

I feel similarly when I learn a recent university graduate is working at McDonalds just like they were in high school. The only difference is that they have a 4-year university degree and are $30,000 more in debt. The situation here is quite frankly bizarre. This reminds of an ad that I would often see in Hamilton that made me laugh while I was on the bus to and from McMaster University. Brock University was advertising that “98% of [it’s] graduates were employed within 2 years of graduation.” No mention of whether those graduates were employed in their field or a related field or if they were using their degree at all for that employment. So I would always joke “yeah and 50% of them are working at McDonalds or underemployed.” It’s not impressive at all that after 2 years out from school you might finally decide to move out of your parents basement and start working literally any job to pay your students loans back. I knew it was bad 5 years ago, and it’s only gotten worse thanks to all these knock on effects of the pandemic and other world events.

Why Toronto is the Epicenter:

So back to the question I posed at the top. Why is the employment rate worse in Ontario and Toronto than the rest of the country? The answer lies mainly in the number of people that choose to come to the province. Ontario is the largest province, has the most schools, and brings in the most people. But we also don’t have as diverse of an economy as the US. We are not the profit center of Canada, that honour goes to our silicon valley, Alberta and their oil. We don’t have the most profitable enterprises in the country, yet we see the most people coming here. Demand to live and work in Ontario and Toronto is much higher than supply, therefore we see the phenomenon’s I have illustrated. This supply-demand imbalance is also somewhat of a contributing factor to all the issues I posed above related to youth unemployment, people leaving Canada, and our false GDP problem, it also underscores the importance of the governments of Toronto and Ontario taking these issues seriously and trying to identify solutions to all these problems. Much of the problem does still lie with the Federal government’s regulations and Bank of Canada policy. But employment, especially for youth, is something I believe needs to be addressed by all levels of government on top of what they’re already doing with housing and population.